Demystifying the Indian Digital Advertising 2020

With the help of Pitch Madison Advertising report 2020, DAN Digital Advertising 2020 report, and GroupM TYNY 2020 report I try to reveal the truth of Indian Advertising Market

Earlier last month when Dentsu Aegis released its annual report Livemint boldly reported - “Digital ad industry to grow 32% to touch 24,920 crores by 2021”. Later when GroupM released its TYNY 2020 report AFAQS reported - “Indian ad spends estimated to grow at 10.7% in 2020”. And now with Pitch Madison Advertising Report out Exchange4Media reported - “Ad market to grow at 10.4%”.

What is my point? There is more to the story beyond the rosy numbers. Majority of the publications have just published the press releases which is half baked truth because they haven’t read the report.

Do a favour to yourself download the report and find out the real truth.

Or you can read my story where I tell you the truth - “Indian advertising is in a recovery mode. Digital is growing but nothing great, it is also recovering. And 2020 will have muted growth because the economy is in a bad state and the 2020 Indian consumer isn’t spending.” (Trust me I have read all the reports)

Read: Hello, marketer, this is what the Indian consumer wants

Indian Advertising - muted growth

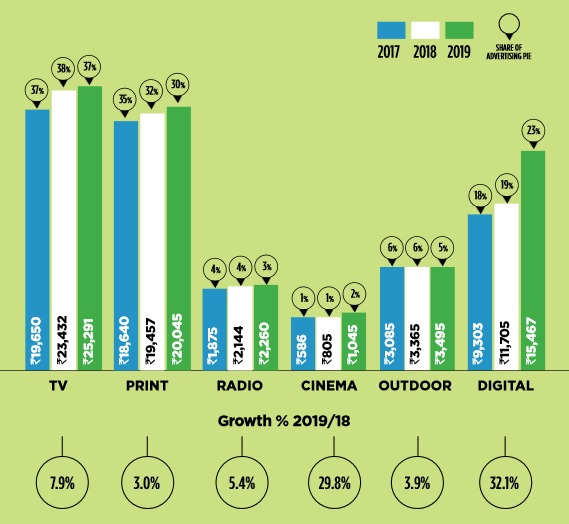

The Pitch Madison Advertising report 2020 released last week gives a timeline of the last three years on how the Indian advertising market has performed. Spend some time with the image and the growth percentage:

The report states: “In 2019, the Media and Advertising industry found itself battling serious headwinds. It started with the largest medium, Televiosion, being badly affected by the New Tariff Order and got further bruised by the wilfull collapse of the growing free-to-air channels by broadcasters.” The festive season was dull with the economy slowing down. The only blip was in Q2, thanks to the IPL, Cricket World Cup and General Elections.

This report estimates that in 2019 Adex grew only at 11% (versus the projection of 13.4% and last year’s growth of 15%), but the figure also hides more than it reveals.

Television, still the largest medium has seen a stagnant growth, Print is down, and all other remaining mediums are in a bad shape. Digital which had an okay last two years is showing growth signs and is the only medium growing. However, growth isn’t encouraging.

Ad spending over the last decade has seen a hit from 2017(53,138 crores), found some respite in 2018(60,908 crores) but went bad again in 2019(67,603 crores).

2020 isn’t looking good.

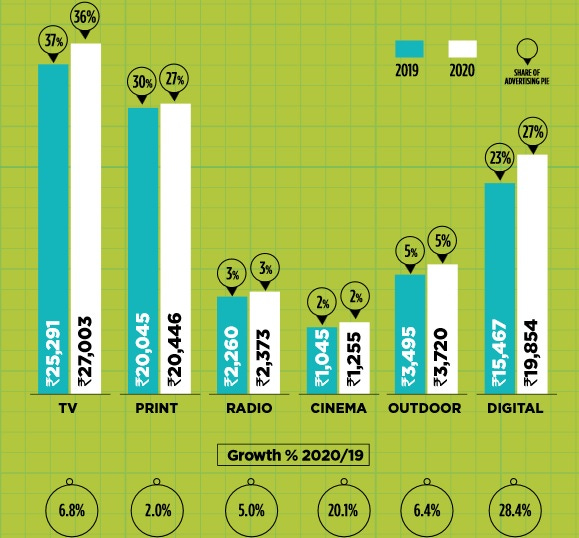

According to the report: “Our forecast for Adex 2020 is muted. In arriving at our projected growth figure for the whole year at 10.4% we are guided by the expectation that the economy should bounce back in the second half of 2020 as indicated in the Government's Economic Survey published on January 31, 2020. We, therefore see a subdued H1 for Adex and buoyant H2, specially Q4.”

In 2020: TV will continue to be the largest medium with a 36% share of Adex but will have a subdued growth rate of 6.8%. Digital and Print will be holding a 27% share of the advertising pie but Digital will witness 28% growth with Print at 2%. However, there is a marginal increase in the percentage of share for Digital from 2019 to 2020.

Cinema, amongst the traditional media, will show a high growth rate of 20%, taking ad spends on the medium to Rs 1,255 crore.

Digital the poster boy

In my earlier story about the DAN Digital Advertising Report 2020, I had highlighted that the Indian advertising market is on a recovery mode.

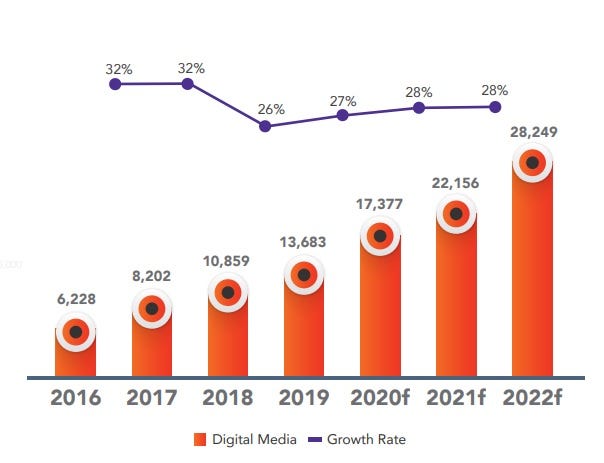

Digital is the medium that is going to witness the strongest growth of 27% in 2019-2020. And hence the medium is the poster boy. The report shared by the end of 2019, the digital advertising industry stood at Rs. 13,683 crores, up at a rate of 26% from Rs. 10,859 crore in 2018.

If you see the above graph the medium has seen a dip from 32% in 2018 to 26% in 2019. Thereafter the projection shows that the medium picks up but the growth percentage is crawling.

Additionally, the DAN report highlighted the fact that the television’s unprecedented reach the medium still owns the largest pie at 39% followed by Print at 39% and Digital at 20%.

While TV’s reach has increased to 96% of the total audience, the time spent has reduced by 21% leading to an average of 11 hours spent per week on TV. And hence it is one of the reasons why it has seen slower growth in 2019 over the last year with its share shrinking from 40% in 2018 to 39% in 2019. The same holds true for print in India - the medium has seen a slower growth with its media spends share declining from 31% in 2018 to 29% in 2019.

Similar trends were observed in the GroupM report - TV still receives the maximum spends and digital has left print behind.

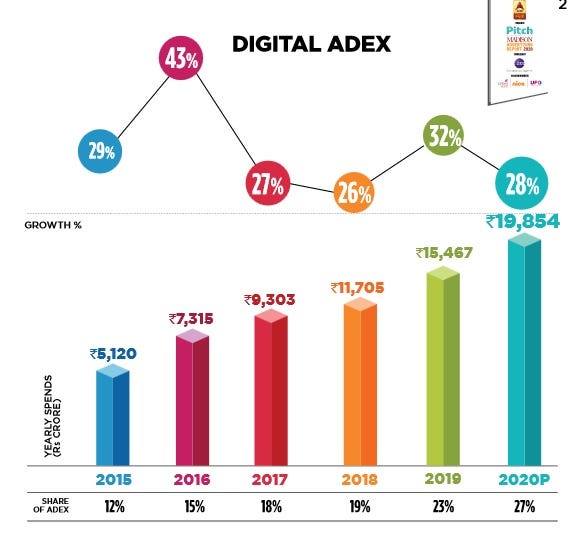

Pitch Madison Report 2020 reveals a similar story. Look at the Digital Adex snapshot:

According to the report: “Digital grew by 32.1% in 2019, adding Rs 3,762 crore to Adex, to reach a size of Rs 15,467 crore. It now contributes a whopping 23% to Indian Adex, with Video advertising steadily gaining ground. Digital is expected to grow by 28% in 2020, to reach Rs 19,854 crore and possibly overtake Print to claim second place next only to Television in Indian Adex”.

But check the growth % - In 2016 it was 43%, after that it got hit and got better in 2018 with 32% but again stands at 28% in 2020(projected). However, the share of Adex has kept on increasing but even that hasn’t been great - 2018(19%), 2019 (23%) and 2020P(27%).

Looking at Digital Adex by various verticals, the report found that it is more or less equally divided between four major segments: Search, Social, Video and Display, with each contributing between 20% to 30% to the total.

Consumption of video is going up year on year and in 2019, video ad spends grew by as much as 59%, beating the Digital Adex growth rate of 32%. The Video vertical is now the highest contributor to Digital Adex at 30%, and almost all of Digital Adex (94%) is on mobile.

Within Online Video, YouTube has the largest share, but OTT is now 20% of the pie and growing faster than YouTube. In Display, GDN has ̃40% share, publishers have 20%.

Currently, e-commerce advertising platforms have made their presence felt at 10% of Display and ad and affiliate networks have the balance. Of the balance 48%, 23% came from Search and 24% from Social. In Search, Google has a virtual monopoly, whereas in Social, Facebook’s absolute dominance is starting to be chipped away by the likes of TikTok and LinkedIn.

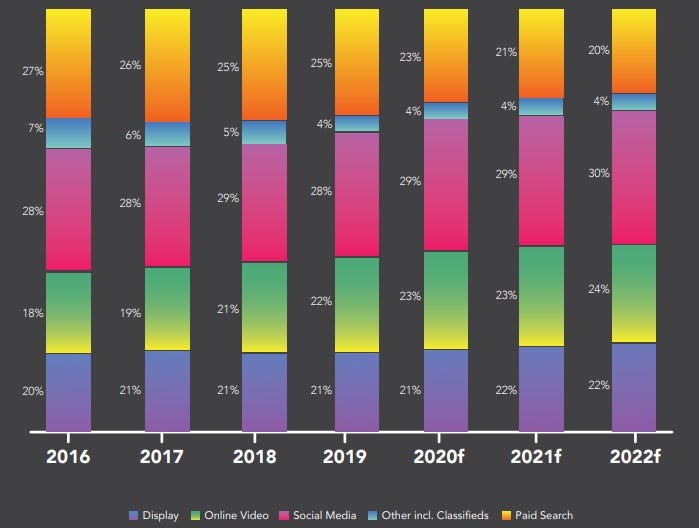

DAN’s report does justice in explaining how different mediums are performing for digital ad spends. Digital Media is led by Social Media with the highest share of 28%, contributing Rs. 3,835 crore to the Indian digital advertising pie. This is followed by spending on Paid Search (23%), Online Video (22%) and Display Media (21%). Display Media, Online Video and Social Media are expected to have the fastest growth in 2020. The share of Paid Search is expected to reduce from 25% to 23% by the end of 2020.

Reasons for the slow growth

(I have shared this in my earlier GroupM TYNY report story)

Overall the Indian advertising spends have taken a set back and one of the reasons has been the Indian economy which hasn’t been in great shape. Indian economy witnessed a slowdown in 2019 and the advertising industry felt the tremors.

Advertisement spends growth rates barely touched 9-10 per cent in 2019 reported The Mint. Compared with a more robust growth rate of 12-13 per cent in 2017 and 2018, though this year was one of the general elections and the cricket World Cup. The market was expecting the dull phase to change during the festive season. But the festival season saw an 8-9 per cent growth in ad spends. Though moderate compared to the 13-14 per cent increase in festival advertising spend last year.

FMCG brands are the biggest investors on TV but thanks to the NTO, most refrained from spending. According to a September report by Credit Suisse, consumer goods companies are likely to post their worst revenue growth in the last 15 years as the slowdown in the sector intensifies due to lower farm incomes, liquidity crunch, and rising unemployment.

With no major events, low consumer demand and a slowdown in sectors, 2020 will have a muted growth.

What is the solution?

Think of your business objective, where the consumer is present and then burn your money on advertising. Don’t just blindly follow trends, mediums and growth stories.

And let's hope the economy will revive.